Convergence of Sequences

Computational Economics (ECO309)

2025-03-27

Life of a computational economist

Life of a computational economist

-

We spend a lot of time waiting for algorithms to converge!

- solution 1: program better

- solution 2: better algorithms

- even better: understand convergence properties (information about the model)

Recursive sequence

Consider a function \(f: R^n\rightarrow R^n\) and a recursive sequence \((x_n)\) defined by \(x_0\in R^n\) and \(x_n = f(x_{n-1})\).

We want to compute a fixed point of \(f\) and study its properties.

Today: Some methods for the case \(n=1\).

Another day:

- the matrix case: \(x_n = A^n x_0\) whre \(A\in R^n \times R^n\)

- the finite nonlinear case: \(x_n = f(x_{n-1})\)

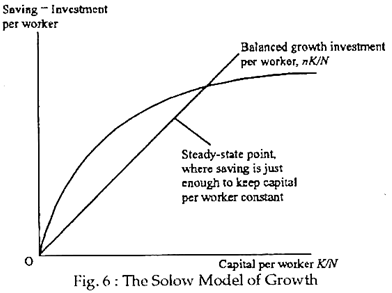

Example: growth model

- Solow growth model:

- capital accumulation: \[k_t = (1-\delta)k_{t-1} + i_{t-1}\]

- production: \[y_t = k_t^\alpha\]

- consumption: \[c_t = (1-{\color{red}s})y_t\] \[i_t = s y_t\]

For a given value of \({\color{red} s}\in\mathbb{R}^{+}\) ( \({\color{red} s}\) is a decision rule) \[k_{t+1} = f(k_t, {\color{red} s})\]

- backward-looking iterations

- Solow hypothesis: saving rate is invariant

Questions:

- What is the steady-state?

- Can we characterize the transition back the steady-state?

- Characterize the dynamics close to the steady-state?

- what is the optimal \(s\) ?

Another example: linear new keynesian model

- Basic New Keynesian model (full derivation if curious )

- new philips curve (PC):\[\pi_t = \beta \mathbb{E}_t \pi_{t+1} + \kappa y_t\]

- dynamic investment-saving equation (IS):\[y_t = \beta \mathbb{E}_t y_{t+1} - \frac{1}{\sigma}(i_t - \mathbb{E}_t(\pi_{t+1}) ) - {\color{green} z_t}\]

- interest rate setting (taylor rule): \[i_t = \alpha_{\pi} \pi_t + \alpha_{y} y_t\]

-

Solving the system:

- solution: \(\begin{bmatrix}\pi_t \\\\ y_t \end{bmatrix} = {\color{red} c} z_t\)

- forward looking:

- take \(\begin{bmatrix}\pi_{t+1} \\\\ y_{t+1} \end{bmatrix} = {\color{red} {c_n}} z_{t+1}\)

- deduce \(\begin{bmatrix}\pi_{t} \\\\ y_{t} \end{bmatrix} = {\color{red} {c_{n+1}}} z_{t}\)

- \(\mathcal{T}: \underbrace{c_{n}}_{t+1: \; \text{tomorrow}} \rightarrow \underbrace{c_{n+1}}_{t: \text{today}}\) is the time-iteration operator (a.k.a. Coleman operator)

-

Questions:

- What is the limit to \(c_{t+1} = \mathcal{T} c_n\) ?

- Under wich conditions (on \(\alpha_{\pi}, \alpha_y\)) is it convergent ?

- determinacy conditions

- interpretation: does the central bank manage to control inflation expectations?

Recursive sequence (2)

Wait: does a fixed point exist?

- we’re not very concerned by the existence problem here

- we’ll be happy with local conditions (existence, uniqueness) around a solution

In theoretical work, there are many fixed-point theorems to choose from.

For instance, we can assume there is an interval such that \(f([a,b])\subset[a,b]\). Then we know there exists \(x\) in \([a,b]\) such that \(f(x)=x\). But there can be many such points.

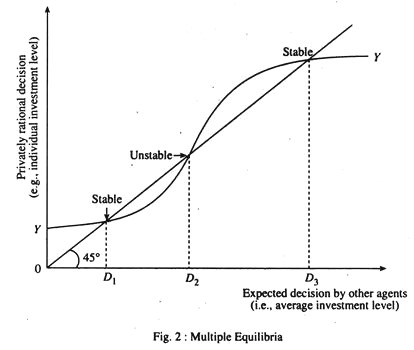

Example: growth model with multiple fixed points

Multiple equilibria in the growth model

In the growth model, if we change the production function: \(y=k^{\alpha}\) for a nonconvex/nonmonotonic one, we can get multiple fixed points.

Convergence

Given \(f: R \rightarrow R\)

How do we characterize behaviour around \(x\) such that \(f(x)=x\)?

Stability criterium:

- if \(|f^{\prime}(x)|>1\): sequence is unstable and will not converge to \(x\) except by chance

- if \(|f^{\prime}(x)|<1\): \(x\) is a stable fixed point

- if \(|f^{\prime}(x)|=1\): ??? (look at higher order terms, details ↓)

To get the intution about local convergence assume, you have an initial point \(x_n\) close to the steady state and consider the following expresion:

\(x_{n+1} - x = f(x_n) - f(x) = f^{\prime}(x) (x_n-x) + o( (x_n-x) )\)

If one sets aside the error term (which one can do with full mathematical rigour), the dynamics for very small perturbations are given by:

\(|x_{n+1} - x| = |f^{\prime}(x)| |x_n-x|\)

When \(|f^{\prime}(x)|<1\), the distance to the target decreases at each iteration and we have convergence. When \(|f^{\prime}(x)|>1\) there is local divergence.

What about the case \(|f^{\prime}(x)=1|\)? Many cases are possible. To distinguish between them, one needs to inspect higher order derivatives.

- when \(|f^{\prime}(x)=1|\), \(|f^{\prime\prime}(x)|\neq 0\) the series will convergence, only if \((x_0-x)f^{\prime\prime}(x)<0\), i.e. starting from one side of the fixed point. The steady-state is not stable.

- When \(|f^{\prime}(x)=1|\), \(|f^{\prime\prime}(x)| = 0\), \(|f^{\prime \prime\prime}(x)|\neq 0\) the series will converge, only if \(f^{\prime}(x)(f^{\prime\prime\prime}(x))<1\)

In general, there is stability only if the function \(f\) is crossing the 45 degrees line (when \(f^ {\prime}(x)=1)\), or the -45 degrees line (when \(f^ {\prime}(x)=1\))

Mathematically, this involves, that:

- the first non-zero coefficient \(f^{k}(x)\) with \(k>1\) has odd order (\(k\) odd)

- it has the right sign

Change the problem

Sometimes, we are interested in tweaking the convergence speed: \[x_{n+1} = (1-\lambda) x_n + \lambda f(x_n)\]

- \(\lambda\) is the learning rate:

- \(\lambda>1\): acceleration

- \(\lambda<1\): dampening

- \(\lambda\) is the learning rate:

- We can also replace the function by another one \(g\) such that \(g(x)=x\iff f(x)=x\), for instance: \[g(x)=x-\frac{f(x)-x}{f^{\prime}(x)-1}\]

- this is the Newton iteration

Dynamics around a stable point

- We can write successive approximation errors: \[|x_t - x_{t-1}| = | f(x_{t-1}) - f(x_{t-2})| \] \[|x_t - x_{t-1}| \sim |f^{\prime}(x_{t-1})| |x_{t-1} - x_{t-2}| \]

- Ratio of successive approximation errors \[\lambda_t = \frac{ |x_{t} - x_{t-1}| } { |x_{t-1} - x_{t-2}|}\]

- When the sequence converges: \[\lambda_t \rightarrow | f^{\prime}(\overline{x}) |\]

Dynamics around a stable point (2)

How do we derive an error bound? Suppose that we have \(\overline{\lambda}>|f^{\prime}(x_k)|\) for all \(k\geq k_0\):

\[|x_t - x| \leq |x_t - x_{t+1}| + |x_{t+1} - x_{t+2}| + |x_{t+2} - x_{t+3}| + ... \]

\[|x_t - x| \leq |x_t - x_{t+1}| + |f(x_{t}) - f(x_{t+1})| + |f(x_{t+1}) - f(x_{t+2})| + ... \]

\[|x_t - x| \leq |x_t - x_{t+1}| + \overline{\lambda} |x_t - x_{t+1}| + \overline{\lambda}^2 |x_t - x_{t+1}| + ... \]

\[|x_t - x| \leq \frac{1} {1-\overline{\lambda}} | x_t - x_{t+1} |\]

How do we improve convergence ?

\[\frac{|x_{t-1} - x_{t-2}|} {|x_t - x_{t-1}|} \sim |f^{\prime}(x_{t-1})| \]

corresponds to the case of linear convergence (kind of slow).

Aitken’s extrapolation

When convergence is geometric, we have: \[ \lim_{x\rightarrow \infty}\frac{ x_{t+1}-x}{x_t-x} = \lambda \in \mathbb{R}^{\star}\]

Which implies:

\[\frac{ x_{t+1}-x}{x_t-x} \sim \frac{ x_{t}-x}{x_{t-1}-x}\]

Aitken’s extrapolation (2)

Take \(x_{t-1}, x_t\) and \(x_{t+1}\) as given and solve for \(x\):

\[x = \frac{x_{t+1}x_{t-1} - x_{t}^2}{x_{t+1}-2x_{t} + x_{t-1}}\]

or after some reordering

\[x = x_{t-1} - \frac{(x_t-x_{t-1})^2}{x_{t+1}-2 x_t + x_{t-1}}\]

Steffensen’s Method:

- start with a guess \(x_0\), compute \(x_1=f(x_0)\) and \(x_2=f(x_1)\)

- use Aitken’s guess for \(x^{\star}\). If required tolerance is met, stop.

- otherwise, set \(x_0 = x^{\star}\) and go back to step 1.

It can be shown that the sequence generated from Steffensen’s method converges quadratically, that is

\(\lim_{t\rightarrow\infty} \frac{x_{t+1}-x_t}{(x_t-x_{t-1})^2} \leq M \in \mathbb{R}^{\star}\)

Convergence speed

Rate of convergence of series \(x_t\) towards \(x^{\star}\) is:

- linear: \[{\lim}_{t\rightarrow\infty} \frac{|x_{t+1}-x^{\star}|}{|x_{t}-x^{\star}|} = \mu \in R^+\]

- superlinear: \[{\lim}_{t\rightarrow\infty} \frac{|x_{t+1}-x^{\star}|}{|x_{t}-x^{\star}|} = 0\]

- quadratic: \[{\lim}_{t\rightarrow\infty} \frac{|x_{t+1}-x^{\star}|}{|x_{t}-x^{\star}|^{\color{red}2}} = \mu \in R^+\]

Convergence speed

Remark: in the case of linear convergence:

\[{\lim}_{t\rightarrow\infty} \frac{|x_{t+1}-x_t|}{|x_{t}-x_{t-1}|} = \mu \in R^+ \iff {\lim}_{t\rightarrow\infty} \frac{|x_{t+1}-x^{\star}|}{|x_{t}-x^{\star}|}=\frac{1}{1-\mu}\]

In practice

- Problem: Suppose one is trying to find \(x\) solving the model \(G(x)=0\)

- An iterative algorithm provides a function \(f\) defining a recursive series \(x_{t+1}\).

- The best practice consists in monitoring at the same time:

- the success criterion: \[\epsilon_n = |G(x_n)|\]

- have you found the solution?

- the successive approximation errors \[\eta_n = |x_{n+1} - x_n|\]

- are you making progress?

- the ratio of successive approximation errors \[\lambda_n = \frac{\eta_n}{\eta_{n-1}}\]

- what kind of convergence? (if \(|\lambda_n|<1\): OK, otherwise: ❓)

- the success criterion: \[\epsilon_n = |G(x_n)|\]